24 Feb HOW TO START A STARTUP

In 2019, most companies considered as tech giants by Forbes had been started as small startups. Facebook that began from a zero-budget private school network or Google that was a research project by two Stanford students is just a couple of examples.

Don’t be ashamed if you don’t have fantastic capital at the beginning. You are not alone! Almost 70% of entrepreneurs in the US launch their startups from college dorms and basements without even renting offices.

This article will teach you what you really need to get started, how to plan your startup development, and avoid critical mistakes made by 60% of startup owners whose projects did not become profitable within 1–4 years since their official business launch.

Why No One Did It Before?

How to start a startup? The very first question you’ve got to ask yourself before any startup activity should sound like “Did anybody implement the same idea before, and if ‘no’ then why?”. The right answer will prevent you from money loss.

Why is its so important? There are millions of creative people who are dreaming about launching a startup at the moment. Some of them may already have launched the same tech startup idea as you’ve got on your mind. If they succeeded, you’ll find them on Google. If they failed, the idea is not demanded. Be attentive! The second is the widest spread reason for startup failure. Last year, it occurred to 42% of startups.

3 steps on how to check your startup idea potential find below.

Check the Need. Is It Real?

You don’t need to hire marketing specialists to conduct market research. Most answers can be found even by non-professionals.

Before building a startup, find out if your idea is worth pursuing by listing the problems it solves. Then try to estimate how many people have those problems and describe them in detail (age, gender, location, and income level). Now you have your specified hypothetical target audience groups.

Get ready for the next step! Imagine yourself being a representative of each of the target groups and estimate how serious listed problems are for you. Use a 10-degree scale where 10 stands for ‘a problem that reduces the quality of my life, I will pay any money to solve it’ and 1 is for a problem that I easily solve myself without even noticing.

If your idea got a high score, move to the next paragraph.

Check Technologies

How to get business ideas? If you could imagine a thing, you could bring it to life, William Arthur Ward once said. However, in the mass tech startup environment, you should also count on technological progress.

If you’ve figured out that your idea is unique and helps people, that may happen that nobody had launched a startup like that before as it would be too costly for them.

Analyze what technologies are required to implement your idea. If they do not exist yet, you need to estimate the development costs first.

Let’s take Uber as an example. In 2009, Uber was launched in the USA as a premium cars taxi service empowered by a regular good-working taxi app. We can presume, that Uber would never have become a global breakthrough taxi on-demand provider, if location tracking technology, mobile internet, smartphones, and online banking hadn’t been improved since 2009. Learn how to build an Uber-like app in our article.

Well, companies like Google can afford to spend dramatic capital on technological research and benefit from global tech progress. Google search engine AI and Google Glass are good examples of such investments. But when it comes to startups, it’s always better to use existing technologies; perhaps, the latest ones.

Check whether your unique idea from the previous paragraph could be based on existing technologies. If ‘yes’, move further.

Check the Market

How to create an idea that will not fail? No market research is the most common mistake made by startuppers. As much as 42% of new tech enterprises failed because just a few people really needed their solutions and were ready to pay for them.

In the business world, everything is money-measurable. Before starting your startup development, get to know how many people can be attracted by your future offer and how much money you can make out of it.

To estimate the market niche volume look through successful cases in similar business fields, study demand trends, and find out niche growth rate. Mind, that there are always some competitors you need to hit. Try to understand if your niche is highly competitive by checking global usage statistics.

For example, it is a bad idea to create an all-in Facebook clone, if there is a constant demand for niche Facebook-like social networks for a particular audience such as pet lovers, religionists, and cross-stitch fans.

How to Create a Startup? Creating a Business Plan Step

What is a tech startup business plan? The document reflects project philosophy, market research results, prior goals and project milestones, general development timelines, and a detailed budget. It also describes the monetization model of an app, project team structure, and an app’s promotional plan.

A business plan is the only way to set off the startup as it is used to present your idea to potential investors and attract them.

In our other blog article, you could find step-by-step instructions on tech startup business plan writing. Here, we’d like to name and describe key startup business plan blocks briefly.

- Executive summary. How to make a business on tech innovations? Start with your mission and then list your key business objectives and goals. Use this section to describe your idea and the way you see the social impact of your startup. Include target group summary and some key market observations taken from the market and customer research as the section also is an introduction one. Add brief information on existed resources, market strategy, and profits.

- Company description and legal structure. Give information on the expert team, its structure and the style it is going to work on the project. Go into details about your existing resources and list extra resources you may need for business launch. List the strengths of your team and give arguments to support the statement that your company is the best one to implement the idea successfully.

- Market research section. To persuade an investor that your idea is worth attention and inspire your team on building a startup, use facts on the current market situation. Show your clear industry understanding describing it briefly. Write down competitors’ names and analyze them, study market trends and measure your chances to obtain your niche. Add target groups description.

- Product description. Explain how your product works and why it is so valuable for the target audience. If your product or service needs to be patented, reflect that fact within the section. Describe the lifecycle of your product and the way you are going to offer it to your future customers.

- Promotional and marketing plan. Give an overview of your marketing strategy. Describe the way you are going to attract and retain users, make them purchase extra product features or sale additional products. Include PR plans and projections there, list some sales strategies you are thinking about.

- Funding section. Business planning for startups should be precise. Outline funding requirements and clarify how much money you need in 6 months, one year, and several years. Explain why you need that exact capital and show how you are going to spend it until you get the first revenue. Present your strategic financial plans (for 5 years or more). In the end, support the request with financial projections, a balance sheet, sales forecast, and a break-even analysis to convince the investor.

Find a Partner

Most of the successful startups were developed not by one person, but by a team. And almost every well-known startup has a least two co-founders. You can’t be an expert in every operating field of your business; startups founded by two or more different experts are more stable compared to others.

Moreover, there are various approaches to forming a foundation team. For example, you may unite with an investor, an experienced marketing specialist, an executive manager, or a niche expert.

How to create a startup? Below, you’ll find some tips on how to pick the right person or to check if the particular candidate is a good choice for you.

Personality

Soft skills are most important while managing the same project. The founders are usually people from whom the corporate communication style starts. Make sure that your partner is comfortable to work with. The best way to do this is to compare your life values and goals.

Skills

How to get business ideas? The right partner could benefit a lot. They may provide you with the necessary pieces of knowledge, experience, and expertise of your target market niche. That person also can help save money on management and marketing. Think of what business skills or knowledge you require to run a startup and find a person who has them.

Work attitude

Bits of knowledge and communicative skills don’t mean a thing if your partner is lacking self-control or doesn’t have any motivation to participate in the working process actively. Ask them several questions on their previous work experience and achievements and be attentive studying their reasons to quit the previous job.

Relations

It’s perfect if you’ve got a long and positive relationship history with your future partner. But don’t be upset if it’s not about you. Try to get as many references on your candidates as you can, speak with their friend circle or families, and decide if you have a chance to build a strong partnership with the person.

A good piece of advice is to create a partnership contract where you can include the financial rights of the founders and describe the way to solve potential crises like the splitting of the company on the owner’s initiative or its shutting down.

Find a Startup Capital

To develop, start and run a startup you need cash. Money is the way to get additional resources such as professional expertise or hard- and software, reach potential users by purchasing promotional campaigns and rent an office to speed up and control startup processes.

According to the latest statistics, 29% of tech startups fail because they run out of cash. Plan your startup budget carefully in order not to become one of them.

A great piece of advice is to create a detailed financial plan and projections that will cover different periods including the next 5 and even 10 years. First, it will prove that you’ve got a serious attitude to your project for investors. And second, that will help you to avoid ‘unexpected’ outcomes soon after startup launch.

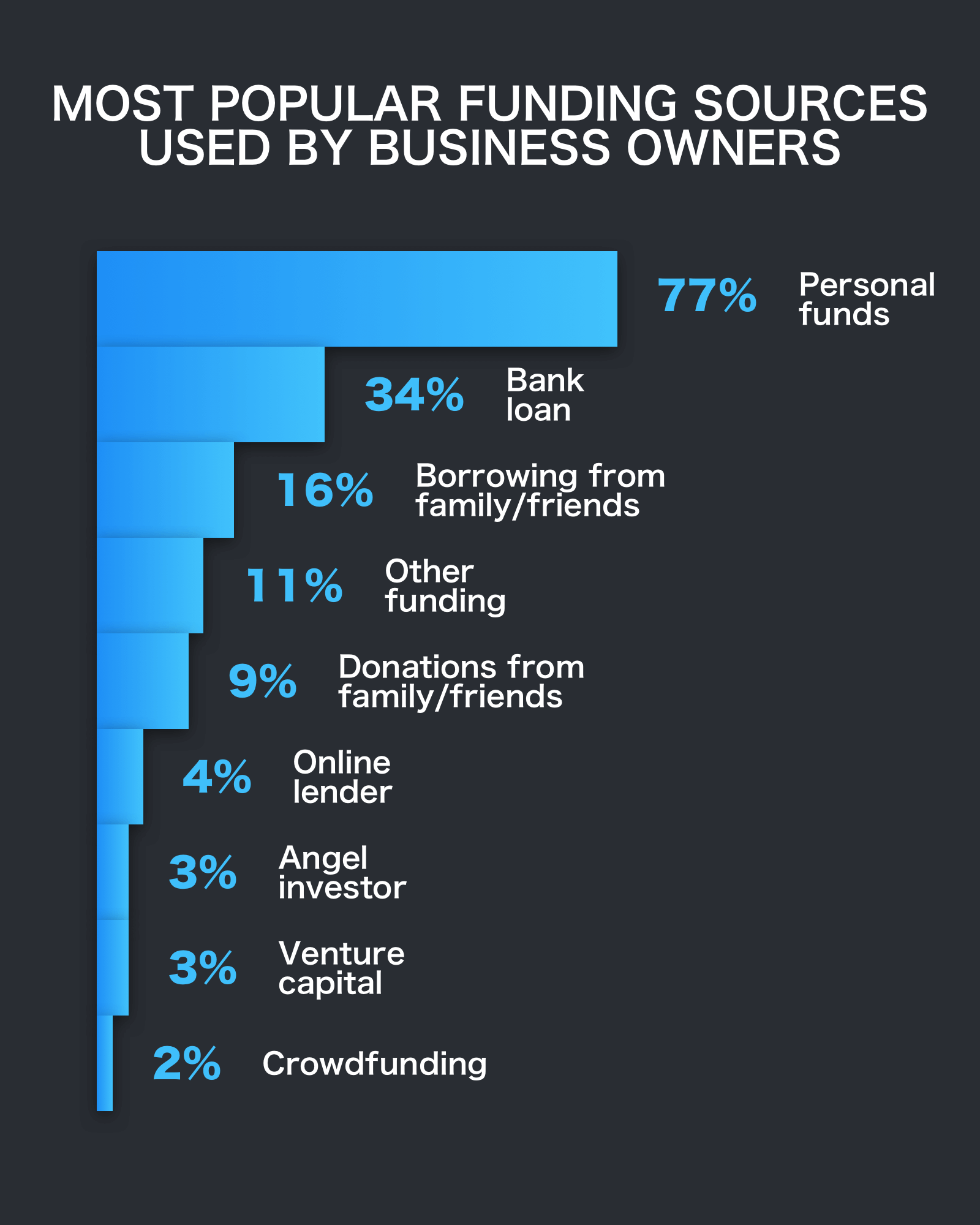

So what’s the best way to raise capital for your project? Below, find the most popular funding sources used by business owners in 2018.

Personal funds (77%)

That is natural that people who come up with the decision to launch a startup are ready for that on every level. They gain relevant knowledge, look for the perfect team, and collect money to take a risk. The last point may cause a problem in the case of web site startup where it’s important to implement an idea before others have done the same.

Collecting money to start your business postpones the launch day and can kill a startup in the bud. However, personal funds give your business independence.

Bank loan (34%)

That is the fastest and the easiest way to provide yourself with the necessary capital. You don’t lose a day as the loaning procedure has been long ago worked in any bank.

There are also some disadvantages to this funding strategy. First, you need to give more money back. Second, you need to present a clear business plan for bank managers. Third, you can’t use this kind of funding if your loan story is spotted.

Family and friends

borrowing money (16%) or getting donations (9%)

Yes, we used to rely on our nearest people and that is natural that most of them are ready to help us. The biggest advantage of relatives-and-friends funding is less strong terms of giving the money back. And the drawback remains a chance to spoil relations with beloved ones.

That is also possible that your friends and family members just don’t have enough money to support the startup. But usually, it is unlikely. In 2019, more than half of all enterprises are started with less than $25,000.

Online lenders (4%)

An online lender is a hybrid of a bank investor and a private one. The person that gives your money doesn’t know you personally and probably would never hear about you if the bank didn’t connect you.

Online lenders provide you with a sort of bank loan using their capital, but it is their banks that support the investing process, take care of the contracts and other documents, and extort compensation from the borrower if he or she doesn’t comply with the terms of the contract.

Angel investors (3%)

It is no coincidence that this term includes the sacred word. Angel investors are the most desirable form of startup financing for its owner. The trick is that such an investor is very difficult to find.

Angel investor is a guardian angel in the business world. The person assumes the costs of starting a startup and its ongoing support, supervises your project, and keeps you from mistakes. Typically, an investor of this type is very interested in the topic of a startup and has sympathy for team members.

Some other less popular funding methods are venture capital and crowdfunding which got 3% and 2%. However, they remain a great source of capital for website startups nowadays, as venture capital and crowdfunding platforms are normally specialized in innovative regional projects.

Find a Mentor

Regardless of the field, the startup process is taking place, having a mentor is a good way to improve your competencies and strive for business excellence. In general, a business mentorship is close to sports coaching. The skills that turn any specialist into a coach are attention to detail and the ability to explain complex things with simple examples.

A business mentor should also be communicative and open-minded, but that is more important for them to speak the same language as you.

In terms of startup mentorship, a mentor’s tasks are the following:

- To supervise startup planning and ongoing management.

- To provide advice for startup funding, team hiring, communication, and general work organization.

- To help with business connections.

- To fill your tech startup knowledge and skillset gaps.

It’s essential to understand that a business mentor is neither a partner nor a teacher. Some business leaders in the tech startup field consider that mentors shouldn’t be top professionals from the area you are working in (however, that is an advantage), but have a definite propensity to observe and manage quality.

Don’t take a mentor’s advice as a direct order. A mentor mission is to provide you with an alternative point of view at your work and fill gaps in your skillset.

Who could be your startup mentor? In fact, anyone. Sometimes, you have mentors even without knowing about it. Friends, relatives, neighbors, and even barmen usually play a mentor’s role in our life: they observe our activities, listen to our daily stories, and give us a piece of advice. The question is who is the best tech startup mentor. Here you’ll find some tips on how to identify this person:

- A mentor shouldn’t be your clone! Look for somebody with another background, set of skills and knowledge.

- Pay attention to the mentor’s networking quality. If the person maintains a connection with professionals, powerful people, or leaders of your area, he or she will bring you extra benefit in the future.

- You should understand each other. No toxic or unconstructive mentorship! At the same time, support diversity as it is a source of useful observations for you.

- Establish a relationship framework. Decide if your mentor will receive a salary or get the percentage of profit; include those points in your business planning for startups documents.

- Find somebody who can conduct mentorship sessions regularly.

The procedure for finding a mentor has no rules. Decide on what mentor you need and go look for him. Of course, your chances of meeting an expert in your industry are higher if you attend professional conferences and seminars. At the same time, sometimes it’s enough just to write to the person you follow on the Internet and invite him or her to supervise your activities.

Other startup steps. Find a Perfect Name

Your startup could have a working title till the moment you need to bring it to market and present it to your target audience. Naming is a part of marketing. Moreover, that is the point where marketing begins.

In our blog, you can find an ultimate tech startup naming guide that will help you to deal with name search quickly and choose the perfect one.

Below, we would like to stop on a few key principles of startup naming. They must be included in the list of steps needed to start a business.

Target audience and marketing study

List things your potential customers like and dislike, find out what gives them emotional pleasure and relief. What problem do you help them to solve and how do they describe it in everyday life? In future stages, try to enrich your name ideas with appropriate positive associations. Look through your competitors and learn how they have solved the name task.

Short, memorable, and easy to spell

More than half of British companies have company name lengths between 7 to 22 characters. But when it comes to tech startup naming you need to consider SEO, Google Play Market, and App Store restrictions. There, the name length should be up to 30 characters.

Lots of startups use only 6–12 letters to describe themselves. Short names with 1–3 syllables are easy to say, which means that people will share information on your project more often.

Make a clear statement. And don’t restrict your development!

In most cases, a name is the first thing potential users hear about you. That’s why it’s important to help them understand what is the idea, mission, and style of your product. If your name is also catchy – be sure they will give priority to you, not competitors.

Remember that a name is an opportunity and not a limitation. Don’t choose names that are too straightforward as they limit your commercial flexibility.

Check the domain name and social profiles

How to make a business that can be promoted with fewer costs? As we said, a name is a part of your marketing. It should help you sell the product. To promote a product successfully, you will need additional promotional platforms. For example, a website on the Internet or a Facebook page where you’ll have a public page with the same name as your product.

If your domain name is taken, it will be difficult for you to get traffic and convert visitors to downloaders. And if an application with the same name already exists, you simply cannot add your product to App Store or Play Market catalog. Use NameMesh to deal with unique name searches.

Create an MVP

An MVP is used by developers to study customers’ needs, preferences, and product usage styles. What is an MVP? A Minimum Viable Product is a ready-made product that includes key functions of your app or another software you’ve been working on.

An MVP development requires less money compared to the end product, so the approach allows founders and managers to avoid resource wasting and stay flexible.

There are several purposes of creating an MVP:

- To get to know if customers really need the product.

- To study what key features of your software are more demanded than others.

- To measure chances to beat competitors.

- To measure users’ readiness to pay for the product.

- To study users’ journey and check the UX concept.

An MVP development which is just a component of the Lean Startup approach by Eric Ries has no differences from any other software development. The idea of the methodology is to build, measure, learn and then repeat actions creating an improvement loop.

It is important to start with considering the essential features of an MVP and proceed with precise planning of your work.

The main strength of an MVP is less time and money required for its launch. Within the approach, you can first test hypotheses related to the feasibility of creating a product in general, and later, hypotheses regarding new functions or design.

Don’t work in a hurry considering an MVP as a draft product, because it is not a draft at all. An MVP development covers a full development cycle, including marketing, tech development, design, and customer support. To create a great MVP, use our detailed MVP guide.

Build-Measure-Learn

“Using the Lean Startup approach, companies can create order, not chaos by providing tools to test a vision continuously”, Eric Ries wrote in his book The Lean Startup: How Today’s Entrepreneurs Use Continuous Innovation to Create Radically Successful Businesses. The author was the first who described a concept of the eternal product improvement cycle in terms of tech startup development.

The Lean Startup idea and its startup steps are based on a scientific approach to startup launching. On the lower level, it operates with such components as Ideas, Code, and Data gained after product launch from users and a support team.

On the higher level it consists of 3 cycled sections: Build, Measure, and Learn. An MVP is an object all Lean Startup activities are focused on, and the Build-Measure-Learn loop helps to minimize the total time spent by the team.

If you are just stepping on the startup ground, get acquainted with the Lean Startup approach first and get down to business after. In the digital industry, the one who embodies his idea earlier than others wins.

Sorry, the comment form is closed at this time.